The Mineral Shortage Is a Growing Problem In The World

Demand for the critical minerals needed to power the energy transition is skyrocketing. Meanwhile, the mining industry is contending with depleted mineral deposits, chronic underinvestment, and environmental and social risks. Rising geopolitical tensions further threaten trade flows and exacerbate the supply gap. And this gap doesn’t just affect the shift to a green economy—it has important implications for advanced technologies as well as broad swaths of the manufacturing sector and industrial base. (Consider, for example, the gargantuan needs of AI and data centers.)

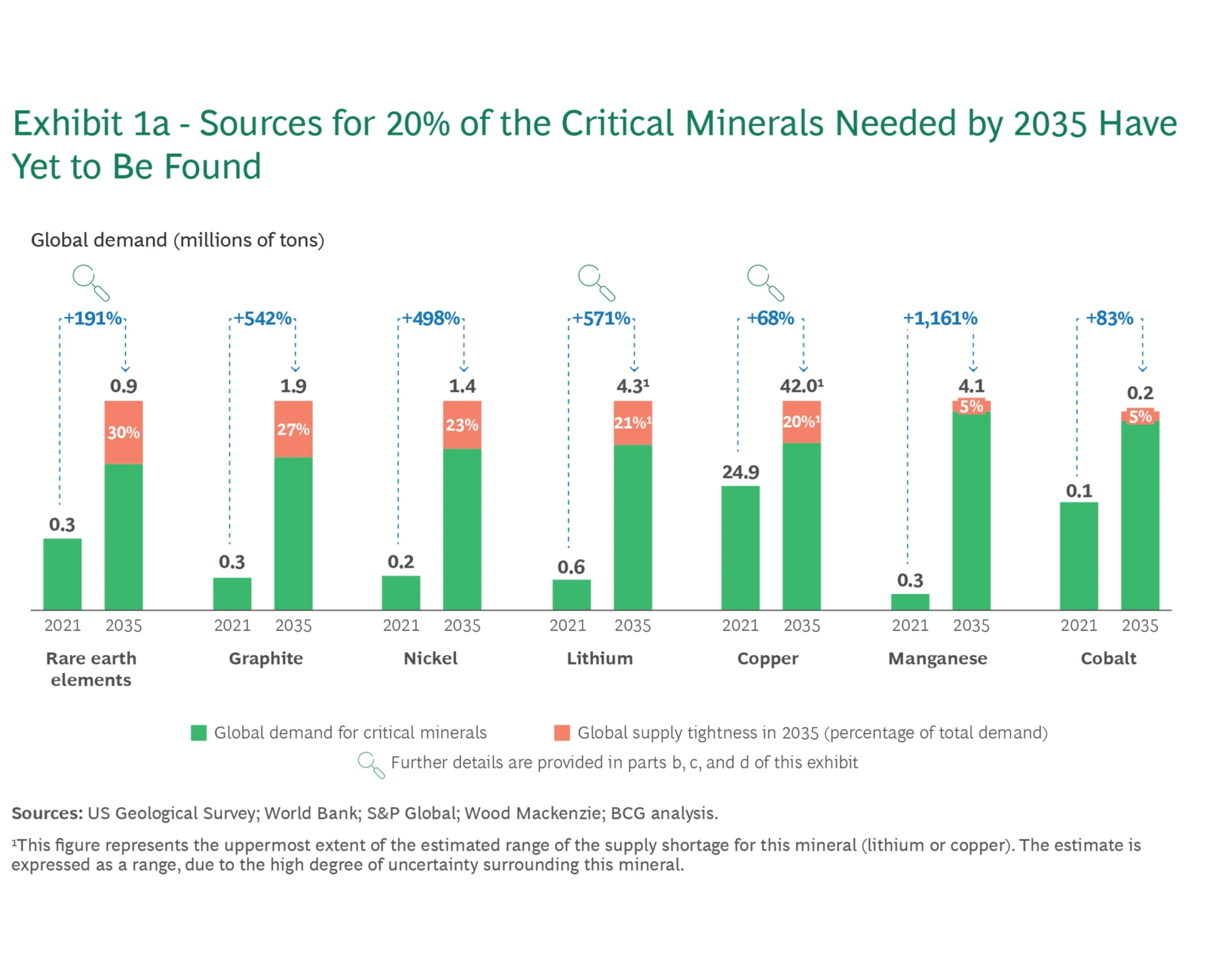

Minerals will be the new oil of the world’s future economy. However, nearly 20% of the total global mineral supply that the world will need by 2035 has yet to be found.

Growing demand coincides with significant geological, operational, and technological constraints, including the depletion of existing mines, a general decline in ore quality, and a shift in new development to riskier regions. Underinvestment in exploration only aggravates these trends. In addition, stricter social and environmental regulations have protracted typical permitting timelines so much that the average time from exploration to first production is now 16 years. Delays can slash a project’s value by over 60%, diminishing its attractiveness to investors and hampering its overall viability.

Export restrictions, reshoring initiatives, and the rise of resource nationalism are intensifying the competition for critical minerals and fragmenting global supply chains. China has tightened its grip on REEs, imposing export bans and leveraging partnerships through the BRICS group of nations to expand its influence.

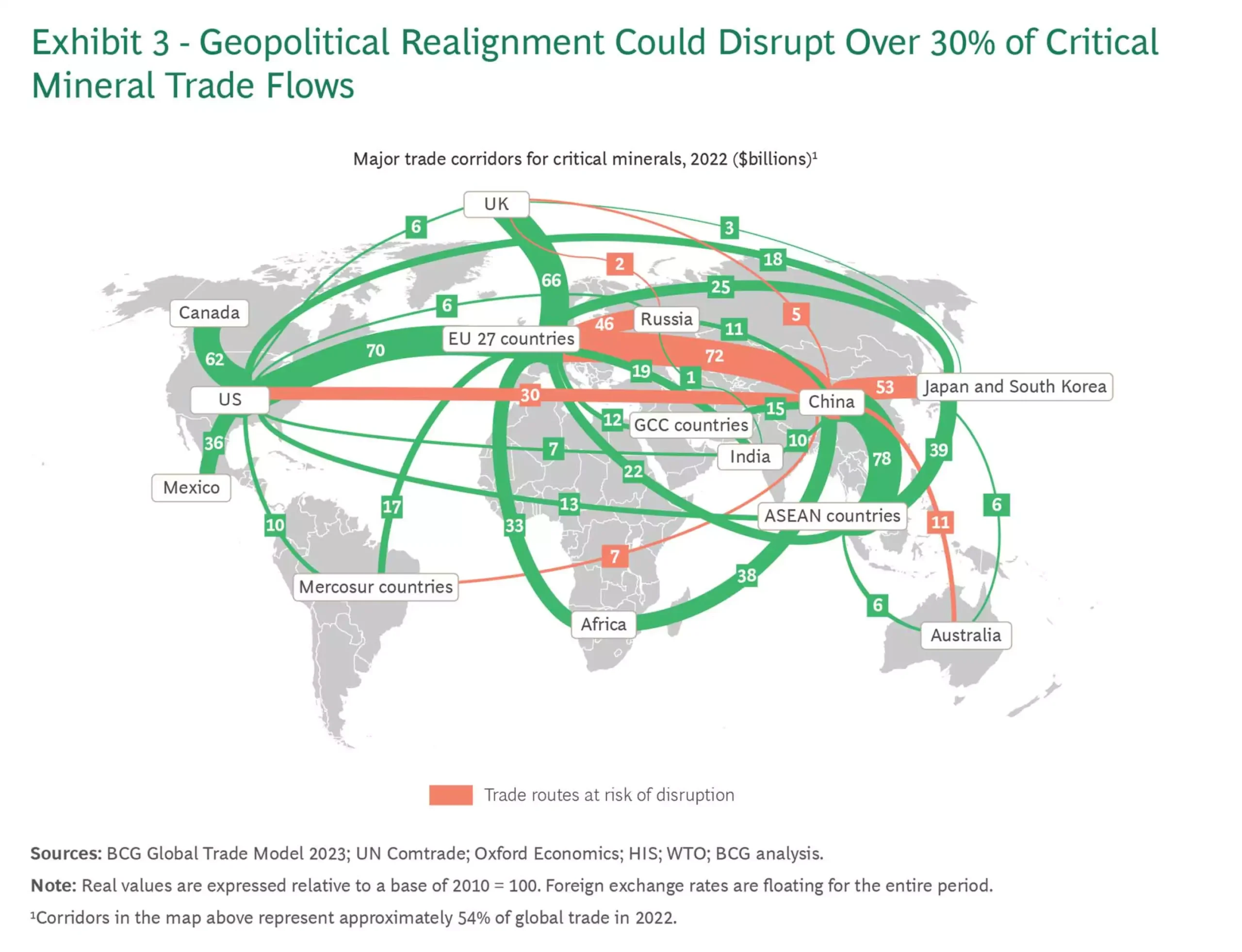

Lately there has been more talk about developing regional supply chains to secure resources and minimize exposure to shocks associated with geopolitical realignment. Such shocks could disrupt around 30% of worldwide mineral trade flows over the next decade, exacerbating supply gaps. Western countries, which rely heavily on mineral imports from resource-rich regions, are particularly at risk.